A Bridge on Economic Issues between China and the World

Facebook

Facebook  Twitter

Twitter  Instagram

Instagram WeChat

WeChat  Email

Email Geographic Imbalances in Access to Credit: The Roles of Branch Networks, Synergies, and Market Power

Concerns about unequal access to credit across regions have become central to policy debates in many economies. Financial integration does not necessarily guarantee that funds flow to areas where credit demand is highest. Instead, geographic frictions, local market power, and institutional constraints may generate persistent “credit deserts”—regions with limited access to external finance despite substantial demand for credit.

A growing body of literature shows that bank finance affects local economic outcomes. Bank integration can promote growth by reallocating funds across regions (Jayaratne and Morgan 2000). Branch networks enable internal liquidity reallocation, smoothing local shocks and supporting lending in high-demand areas (Gilje et al. 2016). Conversely, limited competition can restrict credit supply and distort monetary policy transmission (Drechsler et al. 2017).

We (Aguirregabiria et al. 2025) offer a new perspective on how branch networks, deposit-loan synergies, and local market power jointly shape the geographic distribution of credit. Beyond documenting interregional fund flows, we address a structural question: Which features of the banking system facilitate or hinder the movement of funding from where deposits are raised to where loans are demanded?

Geographic imbalances in deposits and loans

In a frictionless world, deposits collected in one location would flow seamlessly to regions where loan demand is strongest. In practice, however, deposits and loans are often unevenly distributed across space. Some regions generate far more deposits than loans, while others rely heavily on inflows of bank funding from elsewhere.

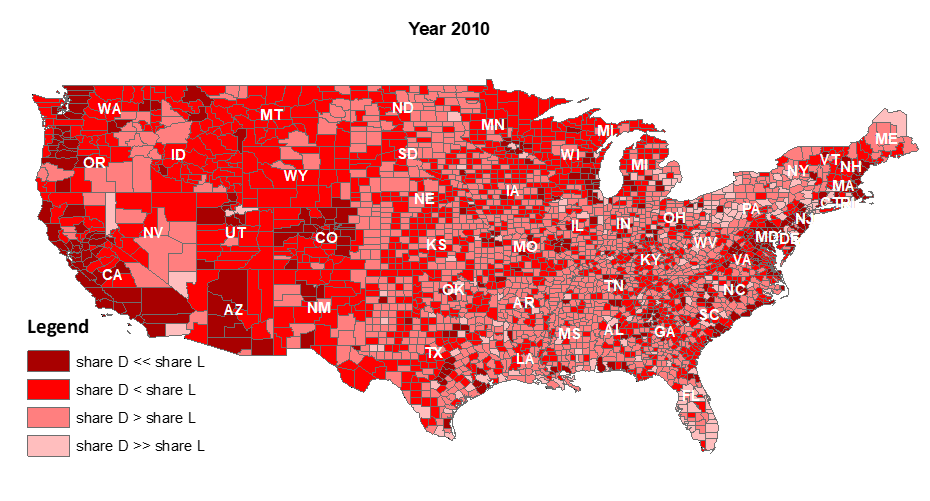

Using county-year data, we document substantial geographic imbalances between deposits and mortgage lending. Figure 1 maps US counties as net borrowers or net lenders of bank funds. For each county-year, we compute its share of national deposits and national mortgage lending; the difference indicates whether it receives more credit than implied by its deposit base (net borrower) or supplies excess funds to other regions (net lender). Counties are grouped by percentiles of this difference to show the direction and magnitude of imbalances across the US. These imbalances are sizable and persistent: Some counties consistently hold disproportionately large shares of deposits relative to loans, while others remain net borrowers.

Figure 1. Geographic Distribution of Net Borrower and Net Lender Counties

Importantly, we do not interpret these imbalances as inherently good or bad. On the one hand, they may reflect efficient financial integration, with funds flowing toward productive investment opportunities. On the other hand, they may signal that certain regions—often smaller, poorer, or more rural—face barriers to accessing credit even when local savings are available.

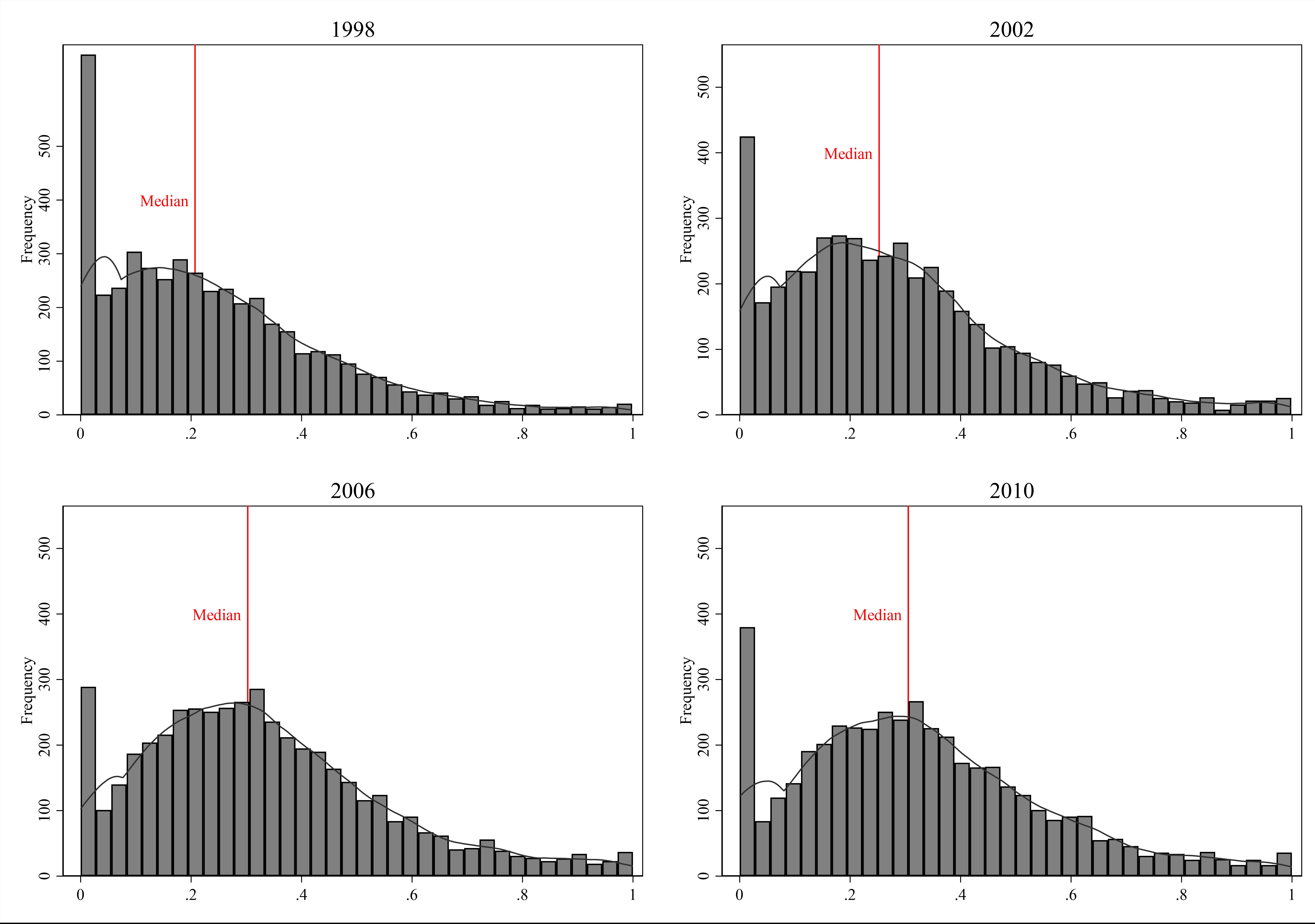

To quantify these patterns, we construct an index of geographic imbalance that measures how far a bank’s distribution of deposits across locations differs from its distribution of loans. A bank with a strong home bias—raising deposits and making loans in the same places—has a low imbalance index (close to 0). A bank that systematically reallocates funds across regions exhibits a high imbalance index (close to 1). This simple metric reveals striking heterogeneity across banks and over time.

Figure 2 presents histograms of the bank-level imbalance index in selected years. While many banks remain highly localized, a non-trivial fraction of institutions actively move funds across regions. Moreover, the extent of geographic reallocation increased following regulatory reforms that led to interstate branching, before declining temporarily during the financial crisis.

Figure 2. Distribution of the Bank-Level Imbalance Index

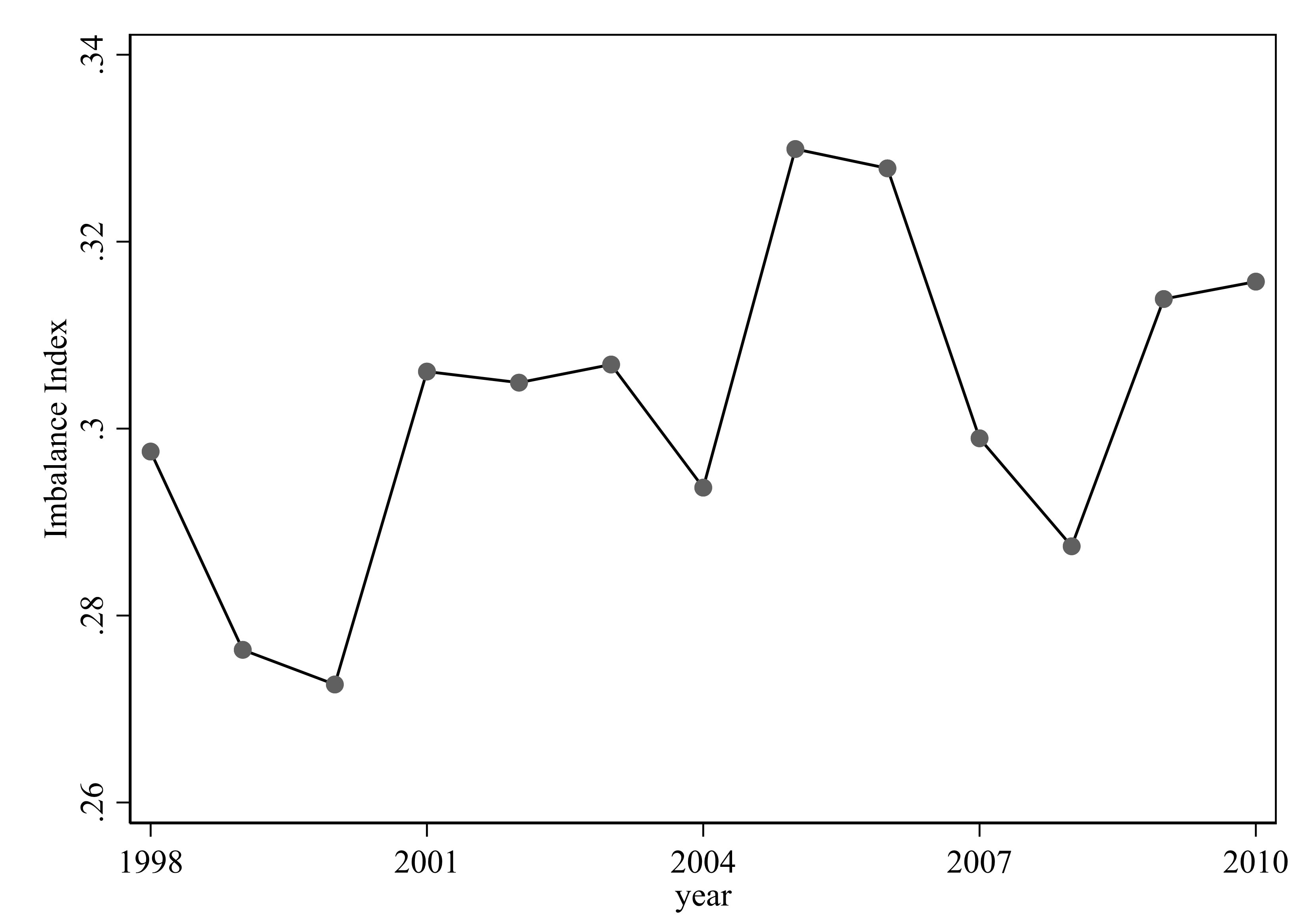

Figure 3 plots a national-level imbalance index that summarizes the geographic mismatch between deposits and lending over time. For each year, the index is computed by comparing each county’s share of total national deposits with its share of total national mortgage lending and aggregating the absolute differences across counties. The time series shows that the imbalance between deposits and lending increases steadily from the late 1990s through the mid-2000s, coinciding with the expansion of interstate branching. The index peaks just before the financial crisis, indicating that a larger fraction of bank funding was being redistributed across regions during the housing boom. During the crisis, the imbalance temporarily declines, reflecting a contraction in interregional credit flows and a retrenchment toward more localized lending.

Figure 3. Evolution of the National Geographic Imbalance Index

Why branch networks matter

Branch networks play a central role in shaping the geographic flow of bank funding. By operating branches in multiple regions, banks can pool deposits internally and reallocate liquidity without relying on wholesale funding markets. This internal capital market can reduce transaction costs, mitigate local liquidity shocks, and expand lending capacity.

Our analysis shows that branch networks are indeed a key driver of geographic credit flows. When banks are allowed to freely reallocate deposits across their branch networks, funding flows more readily toward regions with higher loan demand. Conversely, restricting banks to locally generated deposits substantially reduces the geographic redistribution of credit.

The countervailing role of local synergies

While branch networks facilitate the movement of funds, other forces work in the opposite direction. Banks benefit from providing multiple financial services to the same customers in the same location—so-called “one-stop banking.” These local synergies between deposits and loans can arise from lower operating costs, better information about borrowers, or customer preferences for bundling services. Such local complementarities create incentives for banks to keep deposits and loans together geographically. Even when a bank has excess deposits in one region and strong loan demand elsewhere, local synergies can generate a home bias that limits fund reallocation.

Our results indicate that these local synergies significantly reduce geographic imbalance. Removing them in counterfactual simulations leads to substantially greater flows of credit across regions. This highlights a fundamental tension: The same forces that improve efficiency at the local level can impede the spatial reallocation of capital.

Local competition and credit access

A third critical factor is local market power. Deposit markets are often highly concentrated, especially in small or rural areas, while loan markets—particularly mortgages—tend to be more competitive due to the presence of nonbank lenders.

We show that limited competition in local banking markets significantly constrains the geographic flow of credit. When banks face little competitive pressure, changes in funding costs or internal liquidity are less likely to be passed through to borrowers. As a result, regions with concentrated banking markets receive less credit than they would under more competitive conditions.

This finding speaks directly to ongoing policy debates about competition, regulation, and financial inclusion. Promoting competition in local banking markets may be as important as expanding branch networks in ensuring equitable access to credit.

Securitization and shadow banks

Our results show that securitization and shadow banks play a central role in shaping the geographic distribution of credit. By weakening the link between local deposit availability and lending, securitization allows credit to flow more easily across regions. Shadow banks—non-deposit-taking lenders that rely heavily on securitization—are not constrained by branch networks or local deposit bases and therefore channel credit to high-loan-demand regions where they operate, increasing geographic imbalances between deposits and loans. This mechanism is particularly important in large and urban markets, where shadow banks account for a substantial share of mortgage originations. Counterfactual experiments show that removing shadow banks would sharply reduce lending in these markets and increase the home bias of credit, highlighting their role as a key conduit for interregional liquidity. At the same time, greater reliance on securitization makes credit provision more sensitive to disruptions in secondary markets, with uneven regional effects during periods of financial stress.

Policy experiments

Our structural framework allows us to conduct counterfactual policy experiments that shed light on real-world regulatory issues. We evaluate the impact of restrictions on interstate branching, taxes on deposits, and changes in wholesale funding costs. Policies that limit banks’ ability to operate integrated branch networks can reduce the flow of credit to disadvantaged regions, even if they are intended to promote local lending. Shocks that raise banks’ funding costs—such as higher interbank rates—have geographically uneven effects, disproportionately affecting areas with weaker local competition.

Conclusion

Geographic disparities in access to credit are not merely the result of differences in local demand. They are shaped by the organization of the banking system itself—by branch networks, internal synergies, and competitive conditions.

Our research highlights that branch networks facilitate the geographic flow of bank funding, local synergies create home bias, and market power constrains credit allocation. Understanding these mechanisms is essential for designing policies that promote both financial efficiency and regional equity.

China’s push for a unified national market highlights the importance of cross-regional capital allocation. While nationwide banks with extensive branch networks can, in principle, reallocate deposits across regions, effective capital flows depend on how these networks operate, local deposit–loan complementarities, and competition. As China continues to reform its financial system, careful attention to the geographic dimension of banking may help ensure that savings collected in one region can effectively support growth and opportunity in another.

Victor Aguirregabiria, University of Toronto; Robert Clark, University of Toronto; Hui Wang, Peking University

References

Aguirregabiria, Victor, Robert Clark, and Hui Wang. 2025. “The Geographic Flow of Bank Funding and Access to Credit:

Branch Networks, Synergies, and Local Competition.” American Economic Review 115 (6):. 1818–56. https://doi.org/10.1257/aer.20200374.

Drechsler, Itamar, Alexi Savov, and Philipp Schnabl. 2017. “The Deposits Channel of Monetary Policy.” Quarterly Journal of Economics 132 (4): 1819–76. https://doi.org/10.1093/qje/qjx019.

Gilje, Erik P., Elena Loutskina, and Philip E. Strahan. 2016. “Exporting Liquidity: Branch Banking and Financial Integration.” Journal of Finance 71 (3): 1159–84. https://doi.org/10.1111/jofi.12387.

Jayaratne, Jith, and Donald P. Morgan. 2000. “Capital Market Frictions and Deposit Constraints at Banks.” Journal of Money, Credit and Banking 32 (1): 74–92. https://doi.org/10.2307/2601093.

Latest

Most Popular

- VoxChina Covid-19 Forum (Second Edition): China’s Post-Lockdown Economic Recovery VoxChina, Apr 18, 2020

- China’s Great Housing Boom Kaiji Chen, Yi Wen, Oct 11, 2017

- China’s Joint Venture Policy and the International Transfer of Technology Kun Jiang, Wolfgang Keller, Larry D. Qiu, William Ridley, Feb 06, 2019

- The Dark Side of the Chinese Fiscal Stimulus: Evidence from Local Government Debt Yi Huang, Marco Pagano, Ugo Panizza, Jun 28, 2017

- Wealth Redistribution in the Chinese Stock Market: the Role of Bubbles and Crashes Li An, Jiangze Bian, Dong Lou, Donghui Shi, Jul 01, 2020

- Evaluating Risk across Chinese Housing Markets Yongheng Deng, Joseph Gyourko, Jing Wu, Aug 02, 2017

- What Is Special about China’s Housing Boom? Edward L. Glaeser, Wei Huang, Yueran Ma, Andrei Shleifer, Jun 20, 2017

- Daily Price Limits and the Magnet Effect Ting Chen, Zhenyu Gao, Jibao He, Wenxi Jiang, Wei Xiong, Oct 25, 2017

- Privatization and Productivity in China Yuyu Chen, Mitsuru Igami, Masayuki Sawada, Mo Xiao, Jan 31, 2018

- How did China Move Up the Global Value Chains? Hiau Looi Kee, Heiwai Tang, Aug 30, 2017