A Bridge on Economic Issues between China and the World

Facebook

Facebook  Twitter

Twitter  Instagram

Instagram WeChat

WeChat  Email

Email Expanding Access or Reshaping Markets? Evidence from Public–Private Partnership Health Insurance in China

City-customized supplemental medical insurance (CCSMI) is a major insurance expansion initiative in China through public-private partnership. Although it expanded coverage for hundreds of millions of people, it also crowded out private insurance purchases at both the extensive and intensive margins. This suggests that enrollment growth alone overstates the true gains in risk protection, and calls for better PPP design and stronger coordination with existing insurance programs.

In recent years, building a more effective multitiered medical security system has become a central policy priority in China. Although public health insurance has achieved near-universal coverage, fiscal constraints limit further expansion in benefit generosity, leaving the system primarily focused on basic protection. Out-of-pocket expenditure accounted for 34.4% of total health spending in 2021, significantly higher than the average in OECD countries (WHO 2023).

This leads to growing interest in the role of private insurance in enhancing overall protection. However, voluntary private health insurance markets often face challenges such as limited risk pooling and adverse selection (Rothschild and Stiglitz 1976, Geruso and Layton 2017). These issues are particularly pronounced in China, where the private insurance market remains relatively small. High premiums and limited consumer trust have constrained broader participation.

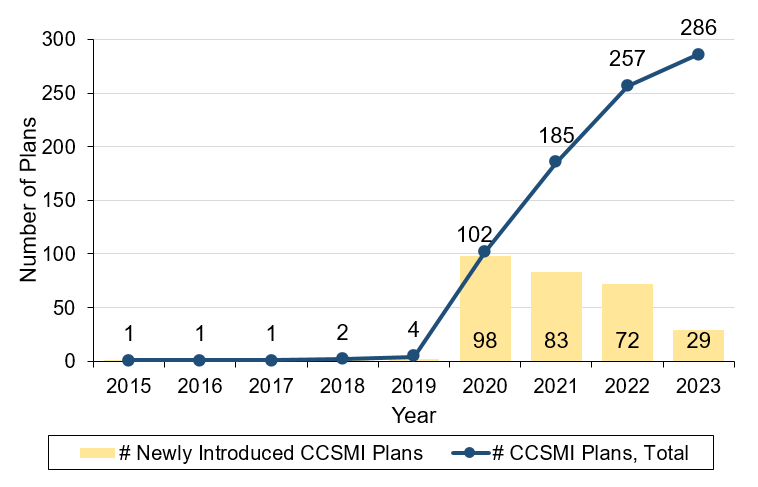

To expand coverage and address the limitations of standalone public and private systems, China introduced city-customized supplemental medical insurance (CCSMI, or “Hui Min Bao”), a government-endorsed, privately operated supplemental insurance program. Following central government guidance in 2020, the program expanded rapidly nationwide. By 2023, over 280 CCSMI products had been launched, covering more than 300 million individuals.

Yet the net effect of this public-private partnered program on coverage expansion remains unclear, as it may partly substitute for existing private insurance rather than fully adding new protection.

City-customized supplemental medical insurance

As an important component of China’s multitiered health insurance system, CCSMI is positioned as a supplemental layer on top of basic public insurance. These plans are typically developed through partnerships between local governments and private insurers at the city level, allowing product design to be tailored to local conditions and the structure of the public insurance system. Local governments primarily play a supervisory and promotional role. Through official endorsement and large-scale outreach, their involvement increases public awareness and trust in the program, which helps expand enrollment and broaden the risk pool, thereby mitigating adverse selection problems. Unlike other public-private partnership programs involving government procurement, there is no direct financial involvement by the government in the operation of CCSMI. However, there may be some indirect support in practice, such as implicit backing or coordination in other forms of collaboration. Meanwhile, private insurers are responsible for designing the products (under government supervision), selling the products, and reimbursing claims.

The key feature of CCSMI is its inclusivity and affordability. Premiums are very low, typically 60 to 150 CNY, with no differential pricing or enrollment restrictions based on age or health status. However, its coverage is also relatively limited compared to traditional private insurance. CCSMI is designed as a supplemental plan for medical expenses covered but not fully paid by public insurance, typically with high deductibles and partial reimbursement for inpatient expenses only. Although some CCSMI plans cover the costs of certain special medications (expensive and not covered by public insurance), and the cap for total annual reimbursement can reach 2 to 4 million CNY, the average payout conditional on successful reimbursement is usually less than 10,000 CNY.

In contrast, private health insurance offers more comprehensive and flexible protection. For example, private medical insurance can provide broader reimbursement for services and medications beyond the list of public insurance covered items. Critical illness insurance typically pays a lump sum—typically over 100,000 CNY—upon diagnosis that can be used for both medical and nonmedical expenses. These plans also charge higher premiums and impose certain health requirements for eligibility.

Figure 1. The Introduction of City-Customized Supplemental Medical Insurance

Note: This figure shows the trend in the number of newly introduced CCSMI plans and the total CCSMI plans in China from 2015 to 2023.

The crowd-out of private insurance

CCSMI is notable for its rapid scale-up and broad participation at low premiums. But what happens elsewhere in the insurance system? In recent work, we examine how this expansion affects private insurance markets by exploiting the staggered rollout of CCSMI across cities (Ding et al. 2026). We combine this policy variation with a transaction-level dataset from a major private insurer, allowing us to track the change in private insurance participation, coverage levels, and premiums before and after the introduction of CCSMI.

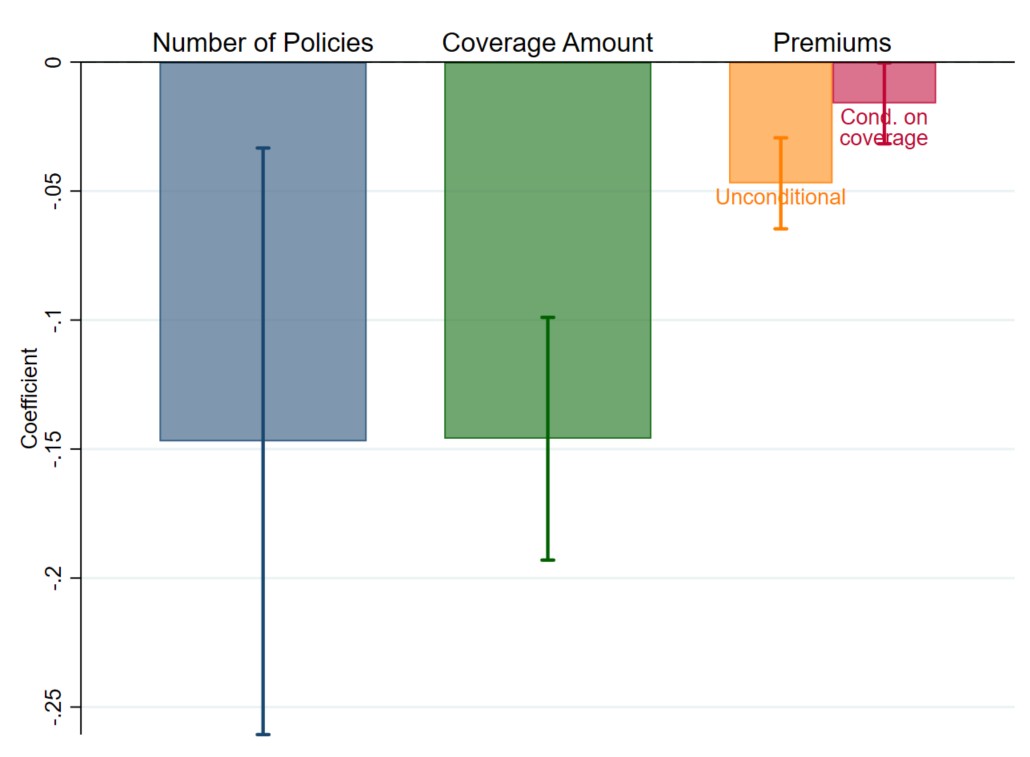

Our findings show clear crowd-out effects in the private insurance market following the introduction of CCSMI. At the extensive margin, private insurance purchases decline by 13.7%. At the intensive margin, among remaining purchasers, coverage levels fall by about 13.6%, and premiums decline by 4.6%. A decomposition of the premium changes suggests that about two-thirds of this decline reflects lower coverage choices, while the remainder implies that insurers adjust prices in response to a more competitive environment.

These results suggest that when access expands through PPP insurance, part of the effect comes from reshaping demand across insurance tiers rather than simply adding entirely new coverage.

Figure 2. The Effect of CCSMI on Private Insurance

Note: This figure shows the effect of CCSMI on private insurance purchases (log number of policies), coverage (log coverage amount), and premiums (log premiums, either unconditional or conditional on coverage amount), based on difference-in-differences estimations. The number of policies is aggregated at the city-month level, while coverage amounts and premiums are analyzed at the individual policy level.

Understanding the net effect of PPP insurance expansion

Comparing the increase in CCSMI enrollment with the decline in private insurance purchases, a back-of-envelope calculation suggests that the reduction in private insurance purchases offsets roughly 25% of the increase in CCSMI enrollment. Since the private insurer we analyze is not a CCSMI-operator, the effect we observe could reflect switching among private insurance products across different insurers. Yet supplemental analysis using aggregated data from all insurers shows similar findings. Overall, these results imply that while PPP insurance expands participation, a meaningful share of the observed growth reflects substitution across insurance tiers. Moreover, since private insurance typically provides more comprehensive protection, this substitution may imply an even stronger crowd-out effect in the level of risk protection.

The design of PPP insurance and its interaction with existing plans matter

Heterogeneity results provide further evidence on when this crowd-out effect is stronger. In cities where CCSMI covers more “special drugs” for cancer treatment, the reduction in the number of private insurance purchases is larger. This is because the indications of these drugs often overlap with those covered by private critical illness insurance. When these drugs are covered by CCSMI, consumers are more likely to view it as a substitute for private insurance and therefore forgo private coverage. Private insurers also adjust prices more in cities where CCSMI provides stronger special-drug coverage, in response to stronger competition.

Meanwhile, in cities with broader special-drug coverage, average coverage amounts become higher among remaining buyers. This suggests that CCSMI with greater overlap in risk protection tends to filter out individuals with lower insurance demand, leaving a pool of remaining buyers with stronger coverage needs on average. This compositional change outweighs the substitution effect at the intensive margin and leads to an overall increase in average coverage amounts.

Policy implications

The direct policy implication is that the expansion of PPP health insurance should be interpreted with care. In the case of CCSMI, increased enrollment does not translate one-for-one into additional insurance protection. Enrollment counts alone are therefore an incomplete metric for evaluating insurance expansion; accounting for crowd-out and coverage structure is essential for understanding overall welfare effects.

Substitution between private and PPP insurance is not necessarily undesirable. Low premiums and nonrestrictive access make CCSMI particularly attractive to groups less well served by existing markets. Given the large coverage gap and limited access to private insurance, the rapid scale-up and broad participation of CCSMI suggest progress toward inclusivity and equity.

However, this may also create sustainability pressures if higher-risk individuals are disproportionately enrolled, while crowd-out may affect the long-term development of the private insurance market. This underscores the importance of better PPP design and stronger integration with existing insurance programs. Future policy should more clearly define the role of PPP insurance in terms of target risks or population groups. Better coordination with existing insurance in benefit structure, reimbursement rules, and pricing may also help mitigate disruptive competition and support a more balanced multitier system.

Information provision is also critical. Prior research shows that individuals often struggle to make optimal insurance choices due to information frictions and tend to focus on salient features such as premiums (Abaluck and Gruber 2011, Handel and Kolstad 2015). This may explain why we observe a larger reduction in total premiums than in enrollment, suggesting that individuals switching to CCSMI may end up with substantially lower risk protection. Improving understanding of product differences and helping individuals align coverage with their needs can enhance the effectiveness of insurance expansion.

Hui Ding, Assistant Professor, School of Economics, Fudan University; Shanghai Institute of International Finance and Economics; Xintong Wang, PhD Candidate, School of Economics, Fudan University; Xian Xu, Professor, School of Economics, Fudan University

References

Abaluck, Jason, and Jonathan Gruber. 2011. “Choice Inconsistencies among the Elderly: Evidence from Plan Choice in the Medicare Part D Program.” American Economic Review 101 (4): 1180–1210. https://doi.org/10.1257/aer.101.4.1180.

Ding, Hui, Xintong Wang, and Xian Xu. 2026. “The Impact of Public-Private Partnership Health Plans on Private Insurance.” Journal of Development Economics 182: 103780. https://doi.org/10.1016/j.jdeveco.2026.103780.

Geruso, Michael, and Timothy J. Layton. 2017. “Selection in Health Insurance Markets and Its Policy Remedies.” Journal of Economic Perspectives 31 (4): 23–50. https://doi.org/10.1257/jep.31.4.23.

Handel, Benjamin R., and Jonathan T. Kolstad. 2015. “Health Insurance for ‘Humans’: Information Frictions, Plan Choice, and Consumer Welfare.” American Economic Review 105 (8): 2449–2500. https://doi.org/10.1257/aer.20131126.

Rothschild, Michael, and Joseph Stiglitz. 1976. “Equilibrium in Competitive Insurance Markets: An Essay on the Economics of Imperfect Information.” Quarterly Journal of Economics 90 (4): 629–49. https://doi.org/10.2307/1885326.

World Health Organization. 2023. “Out-of-Pocket Expenditure as Percentage of Current Health Expenditure, Data by Country.”

Latest

Most Popular

- VoxChina Covid-19 Forum (Second Edition): China’s Post-Lockdown Economic Recovery VoxChina, Apr 18, 2020

- China’s Great Housing Boom Kaiji Chen, Yi Wen, Oct 11, 2017

- China’s Joint Venture Policy and the International Transfer of Technology Kun Jiang, Wolfgang Keller, Larry D. Qiu, William Ridley, Feb 06, 2019

- The Dark Side of the Chinese Fiscal Stimulus: Evidence from Local Government Debt Yi Huang, Marco Pagano, Ugo Panizza, Jun 28, 2017

- Wealth Redistribution in the Chinese Stock Market: the Role of Bubbles and Crashes Li An, Jiangze Bian, Dong Lou, Donghui Shi, Jul 01, 2020

- Evaluating Risk across Chinese Housing Markets Yongheng Deng, Joseph Gyourko, Jing Wu, Aug 02, 2017

- What Is Special about China’s Housing Boom? Edward L. Glaeser, Wei Huang, Yueran Ma, Andrei Shleifer, Jun 20, 2017

- Privatization and Productivity in China Yuyu Chen, Mitsuru Igami, Masayuki Sawada, Mo Xiao, Jan 31, 2018

- Daily Price Limits and the Magnet Effect Ting Chen, Zhenyu Gao, Jibao He, Wenxi Jiang, Wei Xiong, Oct 25, 2017

- How did China Move Up the Global Value Chains? Hiau Looi Kee, Heiwai Tang, Aug 30, 2017