A Bridge on Economic Issues between China and the World

Facebook

Facebook  Twitter

Twitter  Instagram

Instagram WeChat

WeChat  Email

Email Financial Spillovers of Foreign Direct Investment: Evidence from China

Conventional wisdom suggests that FDI can lead to productivity spillovers in host countries, but the benefits of engaging with FDI firms may go beyond productivity. In a recent study, we provide new evidence on financial spillovers of FDI through supply chain linkages. Using Chinese firm-level data, we show that a higher concentration of downstream FDI reduces local suppliers’ trade credit provision and improves their access to bank loans. The trade credit reduction effect is stronger for suppliers serving customers reliant on trade credit or external funding, while the positive bank loan effect is more significant for suppliers facing information frictions. These findings support the case for promoting inward FDI flows in less-developed economies.

Over the past four decades, attracting FDI has been a prominent aspect of China’s state policy of economic openness. Foreign-owned enterprises now play an important role in China’s economy and make substantial contributions to its GDP (Naughton 2018). In the meantime, despite experiencing rapid growth, China’s domestic financial markets remain underdeveloped. Domestic firms, especially those privately owned, encounter severe financial constraints (Dollar and Wei 2007; Song, Storesletten, and Zilibotti 2011). Furthermore, China’s capital control policies limit domestic firms’ access to global financial markets, exacerbating their financial constraints. Extensive evidence suggests that foreign-owned firms possess significant financial advantages over Chinese domestic firms (e.g., Manova, Wei, and Zhang 2015). Given this context, the potential beneficial financial spillovers from FDI become crucial for the growth of Chinese domestic firms and the overall economy.

Conceptually, there are two channels through which domestic suppliers can benefit financially from serving foreign-owned customers. The first channel is trade credit. Firms involved in production chains are financially interconnected through trade credit arrangements (Petersen and Rajan 1997, Fisman and Love 2003). When financially constrained customers delay or default on payments to their suppliers, this can negatively impact the suppliers’ financial conditions (Boissay and Gropp 2013, Jacobson and Von Schedvin 2015, Costello 2020). Foreign-owned customers are generally less financially constrained than their local counterparts. They rely less on trade credit financing and are less likely to delay payments or default. Consequently, serving foreign-owned customers can alleviate domestic suppliers’ burden of trade credit provision.

The second channel is bank loans. Foreign-owned firms often have strong incentives to screen and monitor local suppliers to ensure the stability of their supply chains. For local suppliers, this external monitoring and implicit certification from foreign-owned customers can help mitigate information frictions when accessing credit markets (Cen et al. 2016). By vouching for the reliability and creditworthiness of domestic suppliers, foreign-owned customers enhance the suppliers’ prospects of obtaining bank loans, thereby improving their financial conditions.

Evidence on the Trade Credit Channel

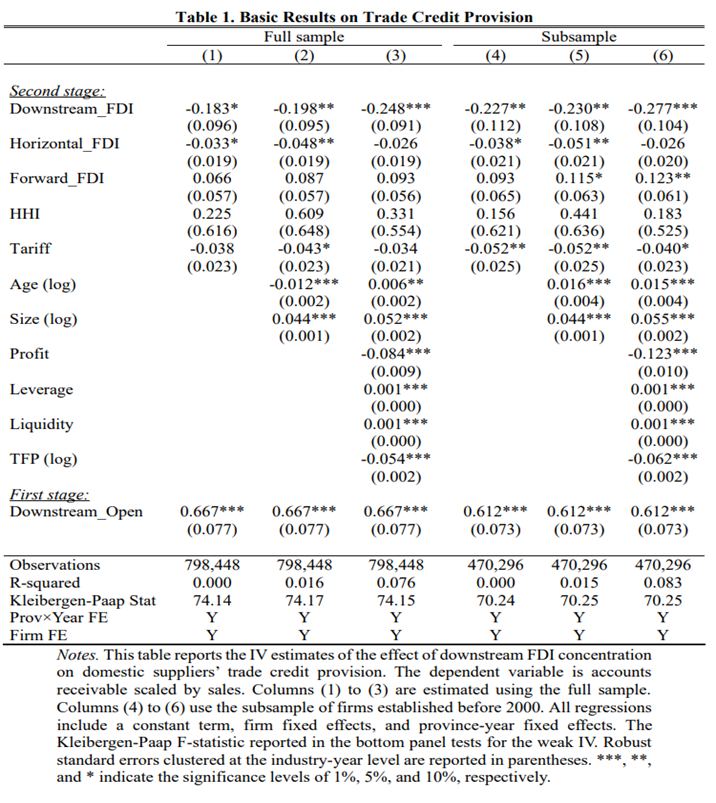

To examine the trade credit channel associated with financial spillovers of FDI through supply chains, we first construct a measure of downstream FDI concentration at the industry level using data on firm ownership and intermediate input usage from the Annual Survey of Industrial Firms, along with import data from China Customs and China’s input-output tables. We then estimate its effect on local suppliers’ accounts receivable (scaled by sales).

To establish causality, we construct an instrumental variable for the measure of downstream FDI concentration, based on China’s FDI liberalization policy following its World Trade Organization accession. To further ensure that our results are not driven by domestic suppliers’ endogenous entry decisions, we also examine the effect of downstream FDI concentration on trade credit provision in a subsample of domestic suppliers established before 2000.

As evident in Table 1, the estimated coefficients on the downstream FDI concentration variable are consistently negative and statistically significant. These findings indicate that a higher downstream FDI concentration significantly decreases domestic suppliers’ trade credit provision.

To strengthen the causal interpretation of our findings, we conduct various analyses to rule out alternative explanations for the observed trade credit effect. Our analyses confirm that the trade credit reduction effect is not a result of FDI’s productivity spillovers, suppliers’ limited credit access, extended payment terms, distrust of foreign buyers, price discrimination, or trade credit reallocation between domestic and FDI customers.

Evidence on the Bank Loan Channel

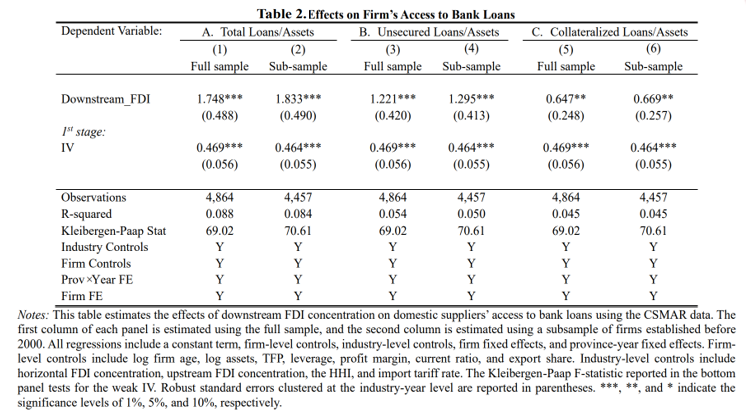

To assess the bank loan channel, we use data on publicly listed Chinese firms from CSMAR and investigate how downstream FDI concentration affects firms’ loan-to-asset ratios. The columns 1 and 2 of Table 2 demonstrate that downstream FDI concentration has a statistically significant and economically meaningful effect on the loan-to-asset ratios of local suppliers. Specifically, a higher concentration of foreign-owned customers in downstream industries significantly enhances local suppliers' access to bank loans.

To gain deeper insights into how downstream FDI concentration affects suppliers’ access to bank loans, we examine the role of information frictions in this relationship. To that end, we decompose suppliers’ total bank loans into collateralized and unsecured loans and analyze the impacts of downstream FDI concentration on each type in the remaining columns of Table 2. Additionally, we explore whether the effect of downstream FDI concentration on bank loans varies among domestic suppliers facing different degrees of information frictions. Our findings consistently demonstrate that the reduction of information frictions, facilitated by serving foreign-owned customers, is a crucial mechanism for enhancing domestic suppliers’ credit access. Furthermore, we dismiss alternative explanations for the bank loan channel, such as productivity spillovers, management skills upgrading, growth potential, and asset downsizing.

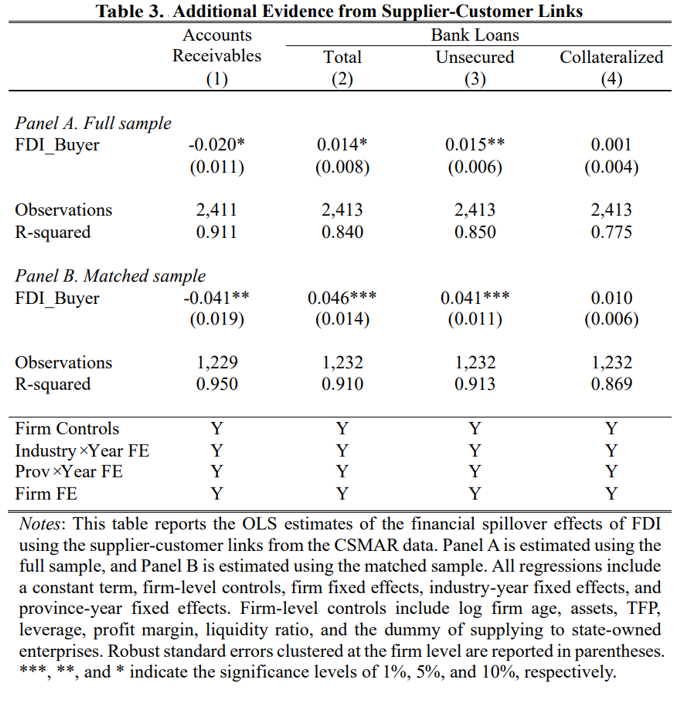

Additional Evidence from Supplier-Customer Links

Finally, we also utilize direct firm-level supplier-customer link information from CSMAR, spanning the period 2009 to 2015 to compare the trade credit provision and access to bank loans between domestic suppliers with foreign-owned principal customers and those without. To address potential bias associated with suppliers’ endogenous choice to engage in transaction relations with foreign-owned customers, we employ a matched firm sample approach to examine the trade credit effect and the bank loan effect based on the nearest-neighbor matching method.

As evident in Table 3, having foreign-owned firms as principal customers can significantly reduce the trade credit provision by local suppliers and substantially improve local suppliers’ access to bank loans. These results thus lend additional support to the beneficial financial spillovers of FDI through the trade credit and bank loan channels.

In conclusion, our analysis using Chinese firm-level data provides robust evidence to support the existence of financial spillovers from FDI through the trade credit and bank lending channels. Serving foreign-owned customers not only alleviates domestic suppliers’ trade credit burden, but also enhances their access to bank loans. These findings shed new light on the financial benefits associated with embracing FDI and hold significant policy implications beyond China.

Considering the pivotal role that finance plays in firm growth and economic development, our findings on the positive financial spillovers of FDI provide an additional justification for advocating openness to inward FDI flows in less-developed countries. By promoting policies that foster an open and welcoming environment for foreign investment, countries can harness the financial spillover benefits of FDI to their advantage.

(Haoyuan Ding, Shanghai University of Finance and Economics; Shu Lin, The Chinese University of Hong Kong; Shujie Wu, Zhejiang University; Haichun Ye, The Chinese University of Hong Kong, Shenzhen)

References

Alfaro-Ureña, Alonso, Isabela Manelici, and Jose P. Vasquez. 2022. “The Effects of Joining Multinational Supply Chains: New Evidence from Firm-to-Firm Linkages.” Quarterly Journal of Economics 137 (3): 1495–1552. https://doi.org/10.1093/qje/qjac006.

Blalock, Garrick. 2001. “Technology from Foreign Direct Investment: Strategic Transfer through Supply Chains.” Empirical Investigations in International Trade Conference, Purdue University.

Blalock, Garrick, and Paul J. Gertler. 2008. “Welfare Gains from Foreign Direct Investment through Technology Transfer to Local Suppliers.” Journal of International Economics 74 (2): 402–21. https://doi.org/10.1016/j.jinteco.2007.05.011.

Boissay, Frederic, and Reint Gropp. 2013. “Payment Defaults and Interfirm Liquidity Provision.” Review of Finance 17 (6): 1853–94. https://doi.org/10.1093/rof/rfs045.

Cen, Ling, Sudipto Dasgupta, Redouane Elkamhi, and Raunaq S. Pungaliya. 2016. “Reputation and Loan Contract Terms: The Role of Principal Customers.” Review of Finance 20 (2): 501–33. https://doi.org/10.1093/rof/rfv014.

Costello, Anna M. 2020. “Credit Market Disruptions and Liquidity Spillover Effects in the Supply Chain.” Journal of Political Economy 128 (9): 3434–68. https://doi.org/10.1086/708736.

Dollar, David, and Shang-Jin Wei. 2007. “Das (Wasted) Kapital: Firm Ownership and Investment Efficiency in China.” National Bureau of Economic Research Working Paper No. w13103. https://doi.org/10.3386/w13103.

Fisman, Raymond, and Inessa Love. 2003. “Trade Credit, Financial Intermediary Development, and Industry Growth.” Journal of Finance 58 (1): 353–74. https://doi.org/10.1111/1540-6261.00527.

Havranek, Tomas, and Zuzana Irsova. 2011. “Estimating Vertical Spillovers from FDI: Why Results Vary and What the True Effect Is.” Journal of International Economics 85 (2): 234–44. https://doi.org/10.1016/j.jinteco.2011.07.004.

Jacobson, Tor, and Erik von Schedvin. 2015. “Trade Credit and the Propagation of Corporate Failure: An Empirical Analysis.” Econometrica 83 (4): 1315–71. https://doi.org/10.3982/ECTA12148.

Javorcik, Beata Smarzynska. 2004. “Does Foreign Direct Investment Increase the Productivity of Domestic Firms? In Search of Spillovers through Backward Linkages.” American Economic Review 94 (3): 605–27. https://doi.org/10.1257/0002828041464605.

Manova, Kalina, Shang-Jin Wei, and Zhiwei Zhang. W. 2015. “Firm Exports and Multinational Activity under Credit Constraints.” Review of Economics and Statistics 97 (3): 574–88. https://doi.org/10.1162/REST_a_00480.

Naughton, Barry. 2018. The Chinese Economy: Adaptation and Growth. Cambridge, MA: MIT Press.

Petersen, Mitchell A., and Raghuram G. Rajan. 1997. “Trade Credit: Theories and Evidence.” Review of Financial Studies 10 (3): 661–91. https://www.jstor.org/stable/2962200.

Song, Zheng, Kjetil Storesletten, and Fabrizio Zilibotti. 2011. “Growing Like China.” American Economic Review 101 (1): 196–233. https://doi.org/10.1257/aer.101.1.196.

Latest

Most Popular

- VoxChina Covid-19 Forum (Second Edition): China’s Post-Lockdown Economic Recovery VoxChina, Apr 18, 2020

- China’s Great Housing Boom Kaiji Chen, Yi Wen, Oct 11, 2017

- China’s Joint Venture Policy and the International Transfer of Technology Kun Jiang, Wolfgang Keller, Larry D. Qiu, William Ridley, Feb 06, 2019

- The Dark Side of the Chinese Fiscal Stimulus: Evidence from Local Government Debt Yi Huang, Marco Pagano, Ugo Panizza, Jun 28, 2017

- Wealth Redistribution in the Chinese Stock Market: the Role of Bubbles and Crashes Li An, Jiangze Bian, Dong Lou, Donghui Shi, Jul 01, 2020

- Evaluating Risk across Chinese Housing Markets Yongheng Deng, Joseph Gyourko, Jing Wu, Aug 02, 2017

- What Is Special about China’s Housing Boom? Edward L. Glaeser, Wei Huang, Yueran Ma, Andrei Shleifer, Jun 20, 2017

- Privatization and Productivity in China Yuyu Chen, Mitsuru Igami, Masayuki Sawada, Mo Xiao, Jan 31, 2018

- Daily Price Limits and the Magnet Effect Ting Chen, Zhenyu Gao, Jibao He, Wenxi Jiang, Wei Xiong, Oct 25, 2017

- How did China Move Up the Global Value Chains? Hiau Looi Kee, Heiwai Tang, Aug 30, 2017